One of the key concerns of Singaporeans is that as we aged, we might be hit with severe disability and as such do not have enough financial resources to take care of ourselves. Severe disability happens when one cannot perform three out of six of the activities of daily living such as:

- Washing

- Dressing

- Feeding

- Going to the toilet

- Walking

- Transferring (from chair to bed and vice versa)

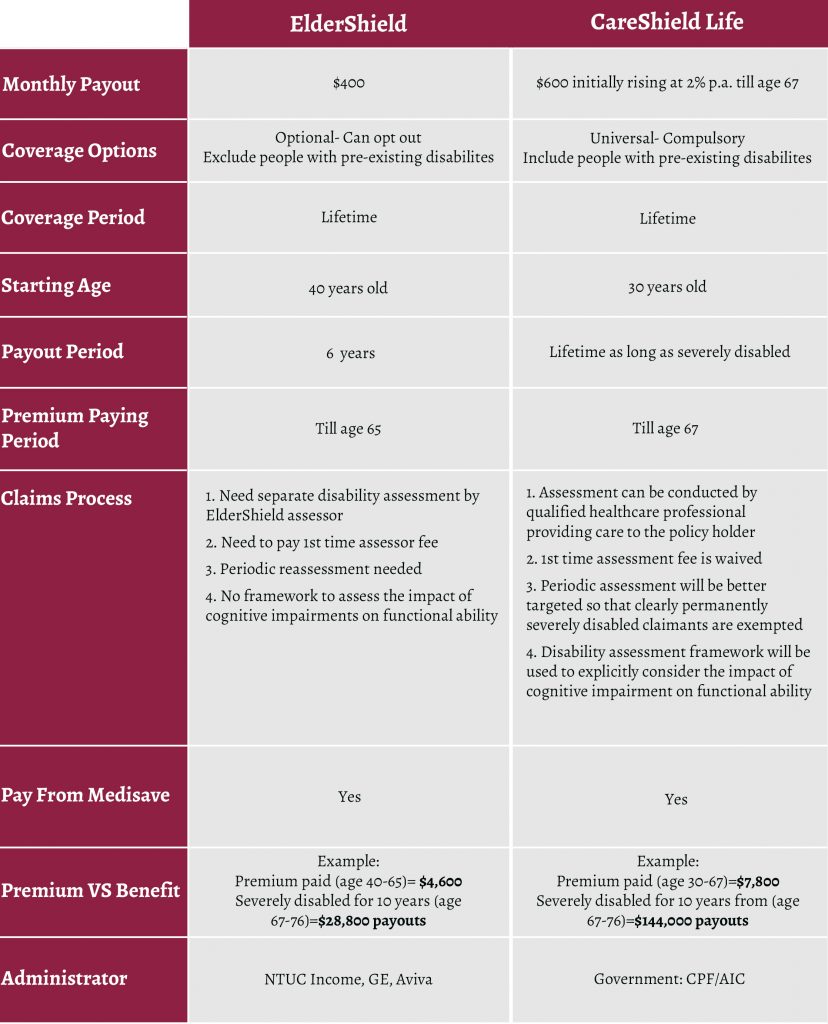

ElderShield is a severe disability insurance scheme to help Singaporeans pay for their long-term care if they become severely disabled. It was launched in 2002. At launch, the plan (ElderShield 300) pays a maximum of $300 per month for 60 months. Subsequently, it was enhanced (ElderShield 400) to pay a maximum of $400 per month for 72 months.

ElderShield is an opt-out scheme. Which means that at age 40, when you are invited to participate in the scheme, if you do not write in to indicate your wish to opt-out, you are automatically enrolled in the plan.

The insurers appointed by Ministry of Health (MOH) in 2002 to operate ElderShield are Great Eastern Life and NTUC Income.

In October 2016, The ElderShield Review Committee was appointed with the task of enhancing the current ElderShield. The review was necessary because Singapore’s need for long-term care will rise with an ageing population. 1 in 2 healthy Singaporeans aged 65 could become severely disabled in their lifetime. While Government subsidies, personal savings and family support will continue to provide significant support, there is room for insurance to play a bigger role in helping Singaporeans prepare for their long-term care needs through risk-pooling. In addition, the current ElderShield payout of $400 per month for 72 months might not be enough as medical cost has gone up over the years and because of advanced medical technology, the severely disabled are living longer.

After almost 2 years of work, the committee announced the enhancements to ElderShield on the 27th May 2018. The new plan will be called CareShield Life when implemented in 2020.

ElderShield vs CareShield Life

The table below shows the key differences between ElderShield and CareShield Life when CareShield Life is implemented in 2020.

The writer, Christopher Tan, is Chief Executive Officer of Providend, a Fee-only Wealth Advisory Firm. Besides being financially trained, he is also an Associate Certified Coach with the International Coach Federation.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.